That “free” weekend can feel like a travel win. You get the resort view, the welcome drinks, maybe a discounted stay in a place you’d never normally book. Then someone invites you to a presentation that’s supposed to last a short while, and suddenly you’re being asked to make a same-day decision about your future vacations.

That moment is where a lot of smart travelers get stuck. The pitch sounds simple. Pay once, vacation better forever. Lock in luxury. Build family memories. Beat rising hotel costs.

The problem is that the cost of timeshares almost never fits on the glossy handout they slide across the table.

A timeshare isn’t just a vacation purchase. It’s a long-term financial obligation tied to one style of travel, one booking system, and a fee structure you usually can’t control. If you love freedom, price shopping, hidden gems, shoulder-season bargains, or changing destinations from year to year, that matters a lot.

Your Dream Vacation or a Financial Trap

A common timeshare story starts with good intentions. A couple takes a beach trip. A solo traveler accepts a resort perk to stretch a tight budget. A family sits down for breakfast and hears they can “own” future vacations instead of “throwing money away” on hotels.

What they’re really deciding in that room isn’t just whether they like the resort. They’re deciding whether they want to commit their future travel money to a product that can be hard to use, expensive to keep, and even harder to leave.

That’s why the most important question isn’t “Can I afford the monthly payment?” It’s “What will this cost me over the full life of ownership?”

For some buyers, the sales pitch gets even more persuasive when exchange options enter the conversation. Being told you can swap into other destinations makes the purchase feel flexible, but exchange systems often sound easier in a presentation than they feel in real life. If you want a grounded look at how swapping works, read this guide to timeshare exchange programs.

A timeshare can look like ownership in the room and feel like a subscription once the bills arrive.

I’m not anti-vacation ownership in principle. I’m pro-clarity. If you understand the numbers, the rules, and the tradeoffs, you can decide from a place of calm instead of pressure. That’s the right way to approach any big travel purchase.

Understanding What You Are Really Buying

The easiest way to understand a timeshare is this: you’re usually not buying a vacation home in the typical sense of real estate ownership. In many cases, you’re prepaying for future stays within a system, while also taking on ongoing owner-style obligations.

That’s why timeshares confuse people. The language sounds like property. The lived experience often feels more like a long contract attached to vacation access.

Deeded ownership and right-to-use

A deeded timeshare usually means you hold an ownership interest connected to the property. That sounds reassuring because the word “deeded” feels close to traditional real estate. But the travel experience still depends on the rules of the resort, the homeowners association, availability, and fees.

A right-to-use timeshare is different. You don’t own a deeded slice of real estate. You’re buying the right to use the property for a period set by contract. That can be easier to grasp if you think of it as a long vacation license rather than an appreciating asset.

In both models, the practical question for travelers is the same. How much real control do you have over where you go, when you travel, and what it costs to keep access?

Fixed week, floating week, and points

Timeshare systems also vary by how you use your stay.

Fixed week means you return to the same property during the same week each year. If you crave ritual and predictability, that may sound comforting. If your work schedule changes or you like chasing cheap flights, it can feel rigid fast.

Floating week gives you a wider booking window within a season or range of dates. That sounds flexible, but flexibility only matters if your preferred dates are available when you try to book.

Points-based systems convert ownership into points you spend across resorts, room types, or travel dates. This looks modern and versatile on paper. In practice, many travelers find points harder to value because the “price” of a trip changes by season, demand, and unit type.

Why this matters for budget travelers

For a flexible traveler, the issue isn’t just cost. It’s opportunity cost. Every dollar tied to a timeshare is a dollar you can’t use to chase a flash sale, stay longer in one city, switch countries, or book a boutique guesthouse with better local character.

Here’s the simplest mental model:

- A house purchase can offer use, control, and equity.

- A hotel booking offers convenience and freedom.

- A timeshare often mixes the obligations of ownership with the limits of a reservation system.

That mix is why so many buyers feel confused later. They thought they were buying certainty. What they often bought was structure.

The Upfront Investment and Initial Purchase Costs

The first number buyers hear is the sticker price. That number is important, but it’s not the whole story. The whole story starts when you add financing, closing costs, and the fact that a timeshare doesn’t behave like a typical appreciating asset.

The price you hear in the room

The average upfront cost of a timeshare in major U.S. markets is around $24,000, and financing often carries 15% to 17% interest. One example cited in this Amerisave analysis of timeshare costs shows that a $24,170 loan at 17% requires $498 monthly payments and adds $17,730 in interest alone, pushing the total cost to over $48,000.

That’s the point many buyers miss. A timeshare that sounds like a mid-range purchase can end up costing about twice as much before you even factor in the ongoing bills of ownership.

Why financing changes everything

Resort financing can make the purchase feel approachable because sales staff focus on the monthly payment, not the total paid. That’s a classic affordability trap. A payment can fit your month and still wreck your long-term travel budget.

Think about what that same cash flow could do elsewhere. It could fund flights during off-peak windows, help you build an emergency travel fund, or let you use one of the best travel rewards credit cards strategically for trips you choose on your own terms.

Practical rule: Never judge a timeshare by the monthly payment. Judge it by the full purchase cost, the contract terms, and what else that money could fund.

Year one is usually higher than expected

Some buyers mentally stop at the sale price. They shouldn’t. The same Amerisave analysis notes that the average transaction price can exclude $2,500 in closing fees, which pushes early out-of-pocket cost higher than many people expect.

A cleaner way to think about year one looks like this:

| Upfront cost piece | What it means |

|---|---|

| Purchase price | The base number used in the sales pitch |

| Closing costs | Extra transaction costs that raise your initial outlay |

| Financing interest | The premium you pay for stretching the purchase over time |

| Immediate loss of value | The gap between what you paid and what the market may later pay |

That last item is where timeshares differ sharply from what buyers often assume. With a car, people expect depreciation. With a timeshare, many buyers are still thinking “property,” “ownership,” or “investment.” That mindset makes the initial purchase feel safer than it is.

The emotional trap in the sales process

Timeshare sales teams are skilled at selling identity, not just lodging. They sell family tradition, better travel habits, and fear of missing out on future prices. That makes the purchase feel emotionally efficient. Buy now, solve vacations forever.

But up front, you’re mostly buying into a system that asks for a lot of money before it proves long-term value for your travel style.

If you need variety, price flexibility, or freedom to skip a year, the upfront commitment often works against you rather than for you.

The Never-Ending Bill of Ongoing Ownership Fees

You sign the papers after a polished sales presentation. A year later, a bill shows up even if you never packed a suitcase. The year after that, it rises again.

That is the part many buyers underestimate. The purchase price gets all the attention, but the ongoing fees decide whether a timeshare fits your real travel budget.

Maintenance fees keep the meter running

Annual maintenance fees are the recurring charge owners feel most. They cover the operating costs of the resort, and they do not disappear just because your travel plans change.

A simple way to view this fee is like a gym membership with a rising annual price, except the bill is usually much larger and tied to a product that was sold as a long-term vacation solution. If you use it heavily, the fee may feel easier to justify. If you skip a year, the cost of every actual night used gets more expensive.

Owners can also face other charges depending on the contract, exchange system, special assessments, or booking rules. The exact mix varies, but the pattern stays the same. Your vacation budget starts with a required bill before you choose where, when, or how you want to travel.

Why these fees sting more than buyers expect

The phrase “maintenance fee” sounds small. It sounds like routine upkeep.

In practice, it acts more like a standing financial obligation. You owe it whether you travel or not, whether airfare spikes or drops, whether your family wants a beach trip or a city break, whether life gets busy or not.

That creates a problem for flexible travelers. A hotel, rental, or off-season deal lets you spend when the trip makes sense. A timeshare asks you to pay first, then shape your vacation decisions around that payment.

Low-use years become very expensive years

The ownership pitch often clashes with real life. Travel habits change.

A new baby arrives. Work gets hectic. A parent needs care. You decide this year is better for a road trip, a cheaper destination, or no major trip at all. The fee still lands in your inbox.

For a budget-conscious traveler, that creates three forms of pressure:

- Less flexibility. Part of your annual travel money is already spoken for.

- Higher cost per trip in skipped years. If you do not use the timeshare, the fee still counts.

- Pressure to force a vacation choice. You may book around the timeshare just to avoid feeling like you wasted money.

That “use it so it feels worth it” mindset is expensive. It can push people away from better-value trips and toward a vacation they would not have chosen on a clean slate.

The real issue is lifetime cost, not the yearly label

A timeshare fee is easy to dismiss when you look at one year by itself. The bigger problem is repetition. Year after year, the charge keeps eating into future travel choices while giving you no equity to show for it.

That is the key difference between the ownership dream and financial freedom in travel. One ties up future cash flow in a fixed system. The other lets you compare prices, change destinations, skip a year, or book a better deal when one appears. If your goal is to travel well without locking yourself into rising obligations, these practical habits for saving money on future trips usually work better than committing to annual ownership costs.

A timeshare can look organized on paper. In real life, the ongoing bill often works like a subscription you cannot easily stop, attached to vacations you may not want to take the same way for decades.

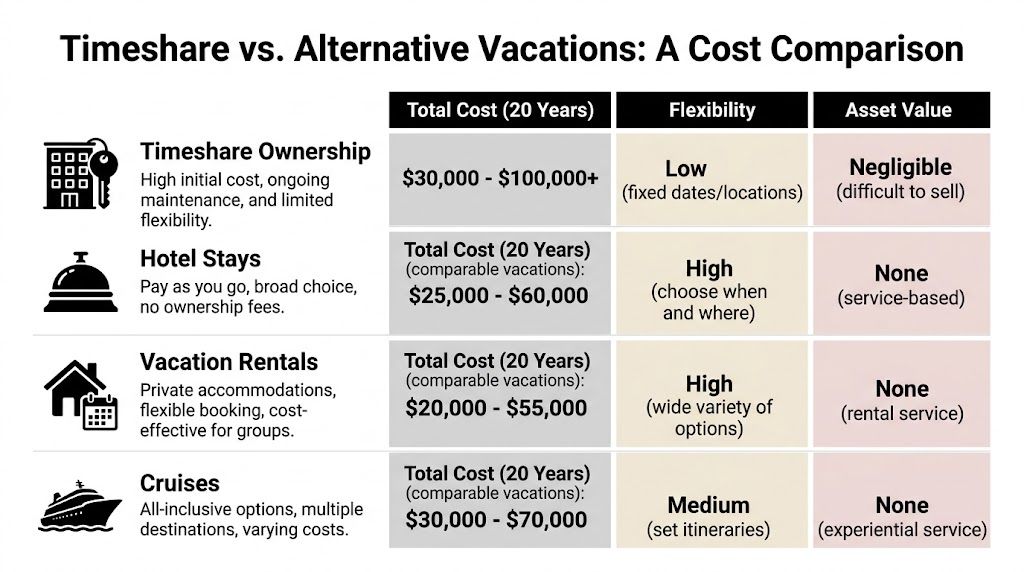

Timeshare Costs vs Alternative Vacation Styles

Two families want a beach week each summer. One signs a timeshare contract and keeps paying year after year. The other books trips one at a time, compares prices, and changes plans when a better option comes along. They may sleep in similar condos, but they are playing by very different financial rules.

That is the comparison that matters.

What the owner is really paying for each stay

A review from Aaronson Law Group on the financial risks of timeshare ownership found effective ownership costs of about $865 per night over 5 years, $612 per night over 10 years, and $547 per night over 20 years. The same review says a comparable timeshare condo can often be rented for about $700 per week, and reports that 85% of timeshare owners express regret.

That gap is hard to ignore. Even if someone keeps the timeshare for decades, the math may still lose to renting a similar stay on the open market.

The sales pitch frames ownership as a way to control vacation costs. In practice, many travelers are prepaying for a system that can still cost more than booking the trip directly.

Side by side, the tradeoff gets clearer

| Vacation Style | Initial Cost | Recurring Cost | Long-Term Cost Pattern |

|---|---|---|---|

| Timeshare ownership | Large upfront purchase | Annual fees that continue and may rise | Builds into a high lifetime travel commitment |

| Renting the same style condo | None | Pay only when you book | Costs track the trips you actually take |

| Discount resort deals | None | Pay only for used stays | Lets you enjoy higher-end trips without a contract |

| Hotels and vacation rentals | None | Varies by destination and season | Easy to adjust up or down based on budget |

A timeshare works like preloading a gift card for one category of vacation, then being charged a service fee every year whether you use it or not. Flexible travel works more like paying cash as needed. You keep the right to compare, skip, switch, or wait for a sale.

That freedom has real financial value, even if it does not show up as a line item on a contract.

Flexibility saves money in ways the brochure does not show

Trip-by-trip booking gives you options that a fixed ownership model limits:

- Wait for airfare or hotel prices to drop

- Pick a cheaper destination in an expensive travel year

- Take a shorter trip instead of forcing a full resort week

- Book a local guesthouse, apartment, or boutique hotel that fits the trip better

- Skip travel for a year without paying ownership costs anyway

Those choices matter most for travelers whose interests change over time. A couple who wanted resort weeks at 35 may want city breaks, road trips, or international stays at 45. A family with school-age kids may travel very differently once those kids are grown.

Why alternatives often fit better

The strongest case against a timeshare is not that vacations should be cheap. Good trips are worth paying for. The problem is paying premium, long-term ownership costs for a style of travel you may outgrow.

A rented condo gives you space and a kitchen without a contract. A hotel gives you convenience without annual fees. Flash sales and package deals can give you the same pool, beach, or resort feel without turning next year's travel budget into an obligation. If that flexible approach fits how you travel, these budget-friendly vacation ideas are a better match than locking yourself into one system.

For the budget-conscious traveler, the biggest advantage is simple. You keep control of your money until you know where you want to go.

The Exit Strategy and Shocking Resale Values

Sales presentations focus on getting in. Smart buyers also ask how to get out.

The timeshare “asset” story often breaks apart. A timeshare may be sold with ownership language, but the resale market often treats it like a burden the next buyer is reluctant to inherit.

Resale value is often brutal

Verified data shows the timeshare resale market is flooded, leading to 95%+ value depreciation. It also notes that many owners end up paying $4,000 to $10,000 to timeshare exit companies just to get out of the contract.

That’s a huge psychological shift for buyers. At purchase, the product is framed as ownership. At exit, many owners discover it behaves more like a liability.

Why the market is so weak

The logic is simple. A resale buyer can often find similar vacation options without taking on old obligations. If they do consider a resale timeshare, they know they have an advantage because so many owners want out.

This creates a harsh mismatch:

- The developer sells a lifestyle at a premium.

- The resale market sees recurring fees and limited flexibility.

- The original owner sits in the middle, trying to recover money from a product many shoppers can bypass.

Exit companies add another layer of risk

When owners realize resale won’t solve the problem, some turn to exit firms. That move can be understandable. People are tired, worried, and eager for a clean ending.

But the very existence of expensive exit services tells you something important about the underlying product. If leaving ownership can cost thousands more, then your total cost of timeshares includes not only buying and holding, but potentially paying to escape.

Before you buy a timeshare, ask the exit question first. “If my life changes, how do I leave, how long does it take, and what does it cost?”

That question belongs in the same conversation as destination perks and room upgrades. If the answer is vague, overly confident, or pushed aside, that’s useful information.

A better way to think about ownership risk

When you’re building a travel budget, you want expenses that stay under your control. You want to be able to scale up in a good year and scale down in a hard one.

Timeshares often do the opposite. They create obligations that can outlive your enthusiasm for the destination, your financial comfort, or your schedule. That’s why many travelers are better served by flexible planning systems and practical travel budgeting tips rather than fixed vacation contracts.

When Does a Timeshare Ever Make Financial Sense

There is a narrow case where a timeshare can make sense. It just doesn’t describe most modern travelers.

A timeshare is most defensible for someone who wants the same type of trip in the same kind of place again and again, values familiarity over exploration, and can comfortably pay cash rather than finance the purchase. That person also needs to accept rising annual fees as part of the deal, not as an unpleasant surprise.

The rare profile that may fit

A buyer is closer to a reasonable fit if they can say yes to most of these:

- They love returning to one resort area. Not “we might.” Not “we like beach vacations in general.” The same place feels like a feature, not a compromise.

- Their schedule is stable. School calendars, work obligations, caregiving duties, and health needs don’t disrupt travel plans often.

- They’ll use it consistently. They won’t resent planning around it.

- They’re not treating it as an investment. They understand it as a consumption purchase.

- They can absorb ongoing fees. The annual bill won’t crowd out savings goals or more meaningful travel.

Who usually shouldn’t buy

If you chase airline deals, prefer shoulder season, travel solo, like trying new neighborhoods, or want your lodging budget to flex with life, a timeshare usually works against your strengths.

For flexible travelers, the better financial move is often simple. Keep your money liquid. Book what you want when you want it. Compare options in real time. Let the market compete for your stay every year.

That approach may feel less glamorous than “owning” your vacations. But financially, freedom is often the more valuable asset.

Frequently Asked Questions About Timeshare Costs

Can I just stop paying maintenance fees

Usually, that’s a bad idea. Timeshare contracts are legal obligations, and resorts may pursue collection or other remedies if you stop paying. If you already own one and the fees have become unmanageable, get the contract reviewed before making any move based on frustration alone.

Can a timeshare become a burden for family members

It can. Some contracts are written in ways that create long-term obligations and family stress, especially when relatives don’t want the property interest or the recurring fees. If you own a timeshare, review the transfer and estate language carefully with a qualified professional so your travel purchase doesn’t become someone else’s problem.

Are vacation clubs different from timeshares

Sometimes in structure, yes. In financial feel, they can be very similar. Vacation clubs may use points, memberships, or broader booking language, which can sound more flexible than a traditional fixed-week timeshare. But the right question remains the same: what are you paying up front, what fees continue over time, how hard is it to book what you want, and what happens if you want out?

What’s the smartest way to evaluate a timeshare offer on the spot

Slow the conversation down. Ask for the full contract, all fee disclosures, cancellation terms, booking rules, and resale or exit language in writing. Then leave. A travel decision that large should survive a night of sleep, a calculator, and comparison shopping.

Is renting always better than owning

Not for every person, but for many travelers it is. Renting protects your flexibility. It also keeps your vacation budget responsive to your actual life instead of a long contract.

Travel should expand your options, not narrow them. If you want practical, budget-smart guidance for planning trips with more freedom and less financial friction, explore Travel Talk Today. It’s a thoughtful resource for travelers who want memorable experiences, stronger budgeting habits, and a travel style that still fits real life.