You get home from a great trip, unpack half your bag, open your banking app, and feel your stomach drop. The meals were small. The train tickets were small. The museum entry was small. But the statement is full of extra charges you never consciously agreed to. They look minor one by one, which is exactly why they slip past people.

That's the trap with international transaction fees. They hide inside convenience. They show up when you tap your card, when you grab cash, and when a payment terminal cheerfully offers to “help” by charging you in dollars. Most travelers assume this is just part of going abroad. It isn't.

The Post-Trip Bill That Ruins the Memories

You usually don't spot the problem while traveling. It shows up later, when your statement turns a good trip into an expensive lesson.

For a lot of travelers, the losses come from a string of small decisions that felt harmless at the time. Tap for coffee. Tap for a train ticket. Grab cash near the hotel. Accept the terminal's “helpful” currency conversion because the screen makes it sound safer. None of those choices feels expensive in the moment. Together, they can chew through a travel budget fast.

One common hit is the foreign transaction fee. As noted earlier, many banks charge around 3% on purchases made abroad. That charge alone can take a noticeable bite out of a longer trip budget, especially if you put most expenses on the wrong card.

What makes this frustrating is how often the extra cost was optional.

Exchange rates move. You can't control that. You can control what happens at the card terminal and the ATM. In my experience, that's where travelers lose the most money without realizing it. The biggest mistakes are rarely dramatic fraud stories. They're routine checkout habits.

Bad payment behavior, combined with the wrong cards, causes more trouble than travel itself. Plenty of travelers research neighborhoods, transit passes, and baggage rules, then pull out the same old bank card overseas and hope it works out. It's the same kind of oversight that leads people to skip the fine print on rentals. The attention to detail behind smart car rental decisions applies to travel money too.

Practical rule: International fees usually come from three choices. Using the wrong card, agreeing to the wrong currency, or taking cash out the wrong way.

That's the part many articles skip. Avoiding international transaction fees is not only about finding a card with the right marketing line on the front. It's also about knowing what to press, what to decline, and what to say when a cashier or ATM gives you a bad option wrapped in polite language. Travelers who spend less abroad are usually the ones who handle those moments well.

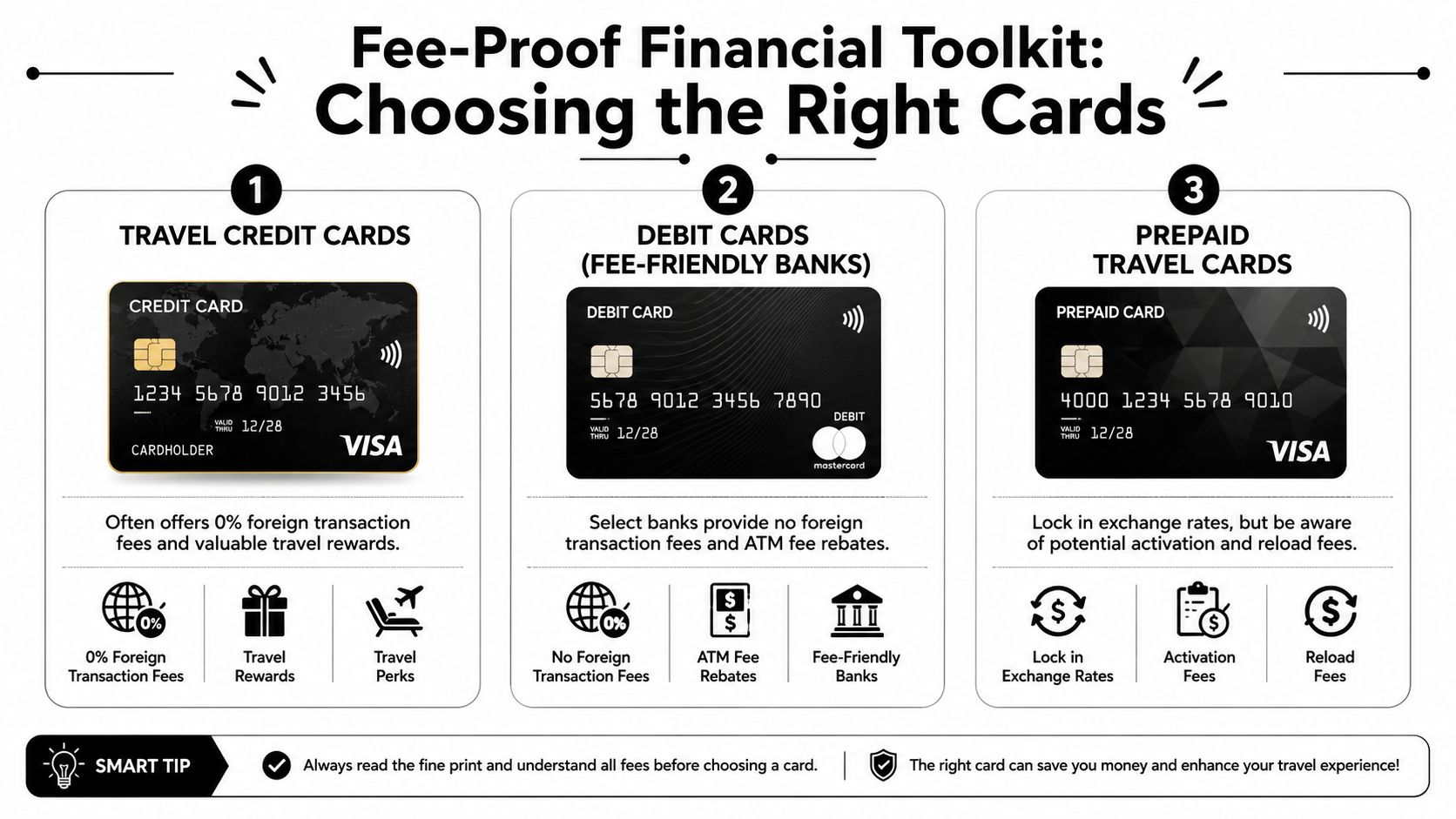

Build Your Fee-Proof Financial Toolkit

A good travel setup separates spending from cash access.

I use different tools for different jobs because travel money problems rarely arrive one at a time. A card gets frozen after an unusual charge. An ATM rejects one network but accepts another. A restaurant takes cards, then the taxi back to the hotel wants cash. The travelers who handle this well are usually carrying a simple setup, not a complicated one.

The core system is a purchase card, a cash card, and a backup.

Use the right card for the right task

For day-to-day spending, use a credit card that clearly says it charges no foreign transaction fee. That keeps routine purchases from picking up an avoidable surcharge. If you are still comparing options, this guide to travel rewards credit cards with strong travel features can help, but I would still check the fee policy before I care about points.

For ATM withdrawals, use a debit card. Credit cards are the wrong tool for cash overseas because cash advances can trigger extra fees and interest. Debit keeps the transaction simpler and easier to track against your checking balance.

Keep those roles separate. It makes fraud cleanup cleaner, and it reduces the odds that one bad card event disrupts every part of your trip.

Here's the visual framework I'd hand any friend before a trip:

The toolkit that works in real life

A practical setup looks like this:

- Primary purchase card: A credit card with no foreign transaction fee and a payment network that works widely where you are going.

- Cash access card: A debit card with reasonable international ATM terms, clear policies, and reliable fraud support.

- Backup card: A second card, ideally on a different network, stored separately from your main wallet.

- Optional travel account: Services like Wise or Revolut can be useful if you want tighter spending control or local currency balances. They are convenience tools. They do not replace reading the fee terms.

That last point matters. Plenty of travelers assume a travel-branded product is automatically cheaper abroad. Sometimes it is. Sometimes it just repackages fees in places people forget to check, such as loading funds, converting balances, or withdrawing small amounts too often.

What usually causes trouble

Prepaid travel cards are often pitched as safer because they limit how much money sits on the card. The trade-off is that some products make up for that with awkward fee schedules. If you have to pay to load money, reload later, or convert currencies, the control starts getting expensive.

I am also skeptical when rewards become the main decision factor. Rewards are nice after the trip. Fee policy affects every purchase during the trip. A plain card with clear terms usually beats a flashy card that turns each restaurant bill into a more expensive transaction.

Your best travel wallet is simple on purpose. One card for purchases. One card for cash. One backup. Clear terms you already checked before takeoff.

A major win is reliability. Once the toolkit is set, the expensive mistakes tend to happen less at account signup and more at the terminal or ATM. That is where good card choices start paying off.

Master the Moment of Payment

The expensive mistake usually happens after you have already done the hard part right.

You picked the right card. You checked the fee terms before the trip. Then a payment terminal in Lisbon, Prague, or Tokyo flips toward you and asks a simple question: pay in local currency or in U.S. dollars. One tap in the wrong direction, and the savings from your fee-friendly card start leaking away.

That screen is usually offering Dynamic Currency Conversion, or DCC.

The habit that saves money fast

Choose local currency every time.

That gives your card network the job of handling the conversion instead of the merchant's terminal provider. In practice, that is usually the cheaper route. The terminal's home-currency option is built to feel reassuring. Familiar does not mean cheaper.

This catches travelers constantly because it shows up in ordinary places. A hotel check-in. A restaurant bill. A souvenir shop. A train kiosk. The mistake feels small in the moment, then shows up later as a worse exchange rate than expected.

What to say at the counter

Keep it short.

“Local currency, please.”

That line works almost everywhere. Say it before the cashier taps anything if you can. If the screen already shows dollars, ask them to cancel it and run it again. If the machine offers a “guaranteed rate” or says “charge in USD,” decline it.

The wording changes. The decision does not.

I also check the screen before I tap my card, not after. That one-second pause has saved me more than once, especially in busy restaurants where staff move fast and assume tourists want their home currency.

How to handle the pushy version

Some merchants will tell you their conversion is better, simpler, or required. It usually is not better for you. It is a revenue add-on for the payment processor.

Stay polite and direct. Ask again for local currency. If they still push, decide whether the purchase is worth it. In places with plenty of alternatives, I would rather walk than overpay. At hotels or larger merchants where you have less flexibility, keep the receipt and review the charge as soon as it posts.

A few spots deserve extra attention:

- Restaurants: Read the terminal screen yourself before tapping.

- Hotels: Ask for local currency at both check-in and checkout.

- Shops: Slow the process down if the cashier is rushing.

- Ticket machines and kiosks: Watch for conversion prompts before you confirm.

- ATMs: Decline any offer to be charged in your home currency.

Some of the worst travel fees look like helpful service.

The good news is that this gets easier fast. After a few transactions, you stop feeling awkward about asking. You are not making a special request. You are asking the payment to be processed the cheaper, standard way.

If you already use travel apps that keep your trip organized, add one more habit to that system: pause, read the screen, and choose local currency before every card payment.

The Smart Traveler's Guide to Withdrawing Cash

You feel the mistake later, not at the ATM. A quick cash withdrawal for snacks, tips, and a train ticket seems harmless until the receipt shows a local ATM fee, your bank adds its own charge, and the machine has pushed an expensive conversion choice on top.

Cash still matters in plenty of places. Small guesthouses, transit kiosks, market stalls, beach bars, and family-run shops may prefer it or require it. The smart move is to treat cash withdrawals like a planned expense, not an errand you repeat every day.

Three costs usually show up at the machine. Your bank may charge for the withdrawal. The ATM owner may charge an access fee. The machine may also offer to bill you in your home currency, which is usually the most expensive choice on the screen.

Use a debit card and make each withdrawal count

A travel-friendly debit card is usually the right tool for ATM access. Credit cards are different. Many issuers treat cash withdrawals as cash advances, which can trigger immediate interest and separate fees. Unless you checked your card terms on purpose and decided the cost is acceptable, skip the credit card.

The practical rule is simple. Withdraw fewer times, and withdraw enough to cover the next stretch of your trip.

That does not mean carrying a reckless amount of cash. It means doing the math before you walk up to the machine. If you expect to need cash for the next few days for transit, tips, small meals, and markets, pull that amount once instead of making three or four tiny withdrawals that each get hit with fixed fees.

What a good ATM withdrawal looks like

A good withdrawal is uneventful. That is exactly what you want.

- Use a bank-operated ATM: Machines attached to actual banks are usually the safer bet.

- Avoid airport and tourist-strip ATMs: Convenience often comes with worse fees and worse exchange options.

- Choose local currency: If the machine offers your home currency, decline it and continue in the local currency.

- Plan your cash needs: One thoughtful withdrawal is usually cheaper than several small ones.

- Set travel alerts and app notifications: Your bank is less likely to freeze the transaction, and you will spot any odd charge faster.

The ATM script that saves money

ATMs often frame the expensive option as the helpful one. The screen may ask if you want the amount converted to dollars, pounds, or your home currency "for certainty" or "guaranteed rate." Decline that option.

Choose to be charged in the local currency. Let your own bank or card network handle the conversion.

I wish more travelers knew how much this one click matters. People spend time hunting for the perfect travel card, then give the savings back at the machine because the ATM wording sounds reassuring.

One more habit helps. Walk a little farther for a bank branch ATM if the first machine you see is in a souvenir shop, convenience store, or airport corner. The nearest ATM is often the most expensive one.

If you want your cash plan to work even better, pair it with a basic trip budget that maps out food, transport, and daily cash spending. That makes it much easier to withdraw the right amount once, store it safely, and stop paying the same fee over and over.

How Small Choices Create Big Savings

Seeing the comparison side by side often prompts a change in habits.

Take two travelers on the same trip with the same $2,000 budget. One uses a standard card, accepts the terminal's dollar conversion, and pulls small amounts of cash several times. The other uses a no-foreign-fee purchase card, pays in local currency, and makes fewer, larger ATM withdrawals.

The difference doesn't come from being richer, more experienced, or more “financially savvy.” It comes from making better decisions at the exact moments fees appear.

Cost Comparison Unprepared vs. Smart Traveler

| Fee Type | Unprepared Alex's Cost | Smart Ben's Cost |

|---|---|---|

| Foreign transaction fee on $2,000 in purchases at 3% | $60 | $0 |

| DCC markup accepted at checkout | Added cost from poor conversion choice | $0 by choosing local currency |

| Repeated ATM fixed fees | Higher total from multiple small withdrawals | Lower total from fewer, larger withdrawals |

| Prepaid card loading or reload fees | Possible extra charges | Avoided by using simpler card setup |

| Total trip friction | Noticeably higher | Noticeably lower |

Why the gap grows fast

The cleanest hard number in that table is the purchase fee. At 3%, a regular foreign transaction fee turns $2,000 of spending into $60 in avoidable cost if you use the wrong card. That follows the same fee structure described by Bank of America's travel payment article.

Once you layer on bad ATM behavior and DCC, the “small stuff” stops being small.

You don't need an extreme trip budget for these decisions to matter. They matter most when your budget is tight, because every extra charge comes directly out of meals, museum tickets, train rides, and one more night somewhere worth staying.

The bigger lesson

The smart traveler doesn't necessarily spend less. The smart traveler loses less.

That's a much better frame for travel money. This isn't about becoming obsessed with every cent. It's about refusing to donate money to banks, ATM operators, and payment terminals when there's no benefit in return.

Saving on fees feels different from cutting joy. You're not shrinking the trip. You're protecting it.

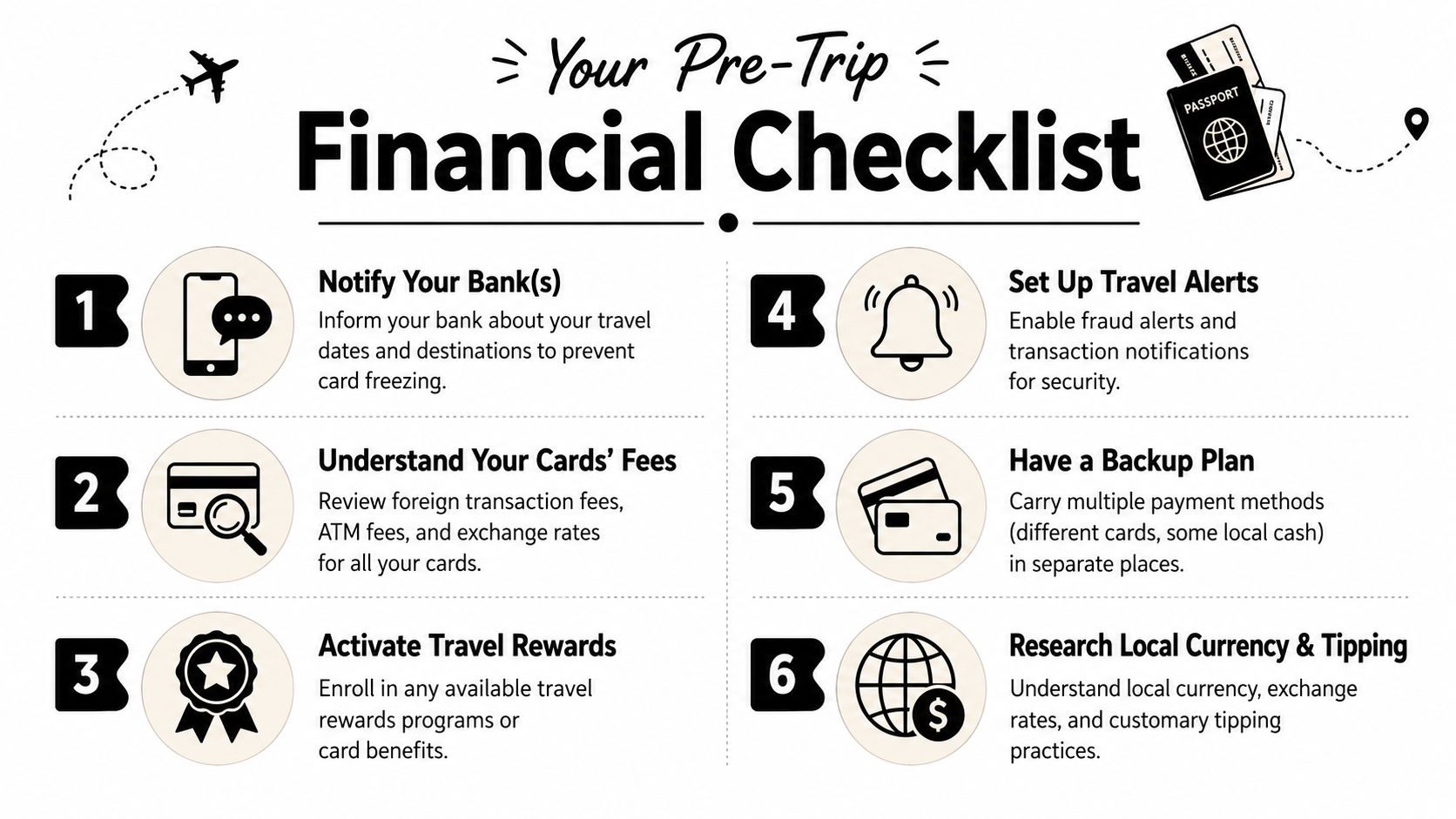

Your Pre-Trip Financial Checklist

The fee mistake that hurts most usually happens when you are tired, rushed, and standing in front of a payment screen you do not fully trust. The fix starts before the trip. Set up your money plan at home, and you will make better decisions in ten seconds at a checkout counter or ATM.

I treat this like packing a passport. If the card setup is sloppy, the trip gets more expensive fast.

What to do before departure

Run through these checks before you leave:

- Pick one card for purchases: Make sure it does not charge foreign transaction fees, then mentally label it your default card abroad.

- Pick one card for cash: Use a debit card for ATM withdrawals, and review how your bank handles overseas ATM use.

- Turn on account alerts: Enable transaction notifications so you can spot a bad charge, duplicate swipe, or suspicious withdrawal right away.

- Block cash advances on your credit card if your issuer allows it: That reduces the chance of an expensive mistake at an ATM.

- Check your daily withdrawal limit: If you plan to make fewer, larger withdrawals, know your cap before you land.

- Carry a backup card in a separate place: A lost wallet should not wipe out every payment option you have.

- Practice the line you will use: “Charge me in local currency, please.”

- Bring a small amount of arrival cash: Enough for transport, water, or a simple first meal, so you are not forced into the first overpriced ATM you see.

That last point saves more trouble than people expect. A little starter cash buys patience. Patience helps you find a bank ATM, avoid a pushy currency conversion screen, and make the first withdrawal on your terms.

Here's the short version worth saving:

The habits worth keeping forever

Good travel money habits should feel boring. You know which card to use. You know what to say at the terminal. You know to pause when an ATM offers a conversion that looks helpful but costs more.

That confidence shows up in small moments. Faster checkouts. Fewer second guesses. Less time staring at a foreign payment screen while a line forms behind you.

If you like leaving home with a written system, this travel planning checklist for trips pairs well with your money setup and helps catch the details that are easy to miss.

Travel should expand your world, not your fee column. If you want more practical, budget-smart guidance from Travel Talk Today , you'll find grounded advice there on planning better trips, spending more intentionally, and keeping more of your money for the experiences that matter.