Let's be honest, comparing travel insurance plans isn't just about finding the cheapest option. It’s about finding the right one for your adventure. The perfect policy for a backpacker hitting remote trails in Patagonia will be completely wrong for a family exploring the cities of Europe. This guide is here to help you see past the price tag and find a plan that gives you true peace of mind on the road.

Your Ticket to Fearless Exploration: Why Insurance Matters

Stop thinking of travel insurance as just another cost. See it as an investment in your own freedom. It's the quiet confidence that lets you say "yes" to that spontaneous jungle trek or a last-minute scuba dive. It turns the fear of what could go wrong into excitement for what’s ahead.

Picture this: you're hiking in the stunning mountains of Peru and a bad fall leaves you with a serious ankle injury. Without insurance, that's a logistical nightmare filled with massive bills and stress. With the right policy, it's just a bump in the road. Your medical costs are covered, and an evacuation is arranged, turning a potential disaster into just another travel story.

That’s the real value of a great plan. It protects your health, your wallet, and your sanity, so you can dive headfirst into every single moment of your trip.

The Shift to Smarter, Safer Travel

Travelers today are more savvy than ever. We understand the risks and want to be prepared. This is why the global travel insurance market, currently valued between USD 22.1 to 27.14 billion, is expected to skyrocket to as high as USD 98.74 billion by 2034. It's not just a passing trend; it's a new standard for responsible adventuring, with European travelers leading the charge. You can find more details about this market growth on imarcgroup.com.

Choosing the right travel insurance is an act of self-reliance. It’s about taking responsibility for your safety so you can embrace the world with an open heart and a clear mind.

This guide isn't about generic tips. My goal is to break down the travel insurance comparison process and help you find a plan that feels like it was made just for you.

- For the Solo Adventurer: We’ll look at policies with strong medical evacuation and generous coverage for your gear. If you're a woman setting out on your own, our guide on how to travel alone as a woman is packed with tips to keep you safe and confident.

- For the Eco-Volunteer: You need a plan that covers you in off-the-grid locations and includes the specific activities you'll be doing—many of which are excluded from standard policies.

- For the Urban Creative: We'll focus on plans with great protection for your expensive camera and laptop, plus solid trip interruption benefits if plans go awry.

By getting into the nitty-gritty and looking at real-world situations, you'll gain the confidence to make a smart, inspired choice. It’s time to unlock a new level of travel freedom.

Cracking the Code: What Really Matters in a Travel Insurance Policy

A travel insurance policy isn't just a document; it's a promise. But to truly understand that promise, you have to look past the marketing slogans and learn to read between the lines. The real art of comparing travel insurance is about translating dense, legal jargon into a clear picture of what will actually happen when things go wrong.

Let's move beyond just ticking boxes. We're going to break down each critical feature from a real traveler's perspective. This way, you'll be comparing plans based on their true value, making sure your policy is a rock-solid safety net, not just another trip expense.

H3: Emergency Medical Coverage: Your Financial First Aid

This is the absolute heart of any travel insurance policy. Why? Because your health plan from back home is often useless the moment you cross international borders. This coverage becomes your primary shield against medical bills that can be financially devastating.

Don't just get dazzled by a big number. Think about where you're going. A policy with $100,000 in medical coverage sounds like a lot, and it might be fine for a trip to Southeast Asia. But that same amount could evaporate in an instant after a serious accident in a country with sky-high healthcare costs, like the United States or Switzerland.

As a rule of thumb, $100,000 is a solid starting point for most international trips. But if you're headed somewhere remote or known for expensive medical care, aiming for $250,000 or more is the smarter, safer bet.

H3: Medical Evacuation: Your Ticket Out of Trouble

This is the unsung hero of travel insurance, and for adventurers, it's non-negotiable. If you get seriously injured trekking in the Andes or exploring a remote island, a regular ambulance isn't coming for you. Medical evacuation is what pays for the helicopter, the specialized plane, or whatever it takes to get you to a facility that can properly treat you.

These rescue operations can easily soar past $100,000. That's not an exaggeration. Seeing a policy with $500,000 or even $1,000,000 in evacuation coverage isn't overkill—it’s a realistic safeguard against a nightmare scenario. When you’re comparing plans, never, ever skim past this number.

A crucial distinction many travelers miss: medical coverage and medical evacuation are two different things. Evacuation gets you to the hospital; medical coverage pays for the care at the hospital. You absolutely need high limits for both.

H3: Trip Cancellation & Interruption: Protecting Your Investment

Life is what happens when you’re busy making other plans. Trip cancellation reimburses your prepaid, non-refundable expenses—like flights and tours—if you have to scrap your trip for a covered reason before you even leave.

What's a "covered reason"? It’s usually the big stuff:

- A sudden, serious illness or injury to you, your travel buddy, or a close relative.

- An unexpected death in the family.

- A natural disaster that makes your destination unsafe.

- Being called for jury duty.

Trip interruption is its sibling, kicking in after you’ve already departed. It covers you if you have to cut your trip short for similar reasons, refunding the unused portion of your trip and often covering the steep cost of a last-minute flight home.

The key is to understand what qualifies as a "covered reason," as this varies between insurers. If you want the ultimate safety net, look for a Cancel For Any Reason (CFAR) upgrade. It costs more and usually only pays back 50-75% of your costs, but it gives you the freedom to back out for, well, any reason at all.

H3: Baggage & Personal Belongings: When Your Gear Goes Missing

Losing your luggage is more than an inconvenience; it can derail the start of your trip. Baggage coverage is designed to help, reimbursing you if your stuff is lost, stolen, or damaged. But the devil is in the details here.

Pay close attention to two numbers: the overall limit (e.g., $2,500) and the per-item limit (e.g., $250). That per-item limit is the catch. It means if your $1,500 laptop gets stolen from your bag, the policy will only pay out $250. If you’re traveling with a nice camera, a drone, or other pricey gear, you need to find a plan with higher per-item limits or get a separate rider to cover your valuables.

It's also worth checking the benefits on your credit card. Some of the best credit cards for travel rewards come with their own purchase and baggage protection that can fill in the gaps.

H3: Adventure Sports & Exclusions: Is Your Fun Covered?

Finally, a policy is worthless if it doesn't cover what you actually plan to do. Most standard plans have a long list of "high-risk" activities they won't cover. This list can include everything you'd expect, like bungee jumping and rock climbing, but sometimes also things you wouldn't, like scuba diving below a certain depth or even just riding a scooter.

Before you click "buy," make a quick list of all the adventures you're hoping to have. Then, search the policy documents for those keywords. If they're on the exclusion list, you'll need to purchase an "adventure sports" or "hazardous activity" add-on. Paying a little extra for this is infinitely better than finding out you're uninsured a moment too late.

At-a-Glance Travel Insurance Feature Breakdown

To help you cut through the noise, here's a quick reference table highlighting the key features and our recommended minimums for two common types of travelers. This should give you a solid baseline for your own comparison.

Remember, these are just starting points. The right coverage is deeply personal and depends entirely on your destination, your health, and your appetite for adventure. Use this as a guide to ask the right questions and find the policy that lets you travel with true peace of mind.

How Policies Actually Perform in the Real World

Policy documents and comparison charts are a great start, but they don't tell the whole story. The true test of any insurance plan is how it holds up when things go sideways on the road. To really get a feel for what matters, you have to imagine how a policy would work for you in a real-life mess.

Let's walk through a few different traveler scenarios. By putting ourselves in their shoes, we can see how certain policy features go from being a "nice-to-have" to an absolute lifesaver. This is how you find a plan that genuinely fits the way you travel.

The Solo Digital Nomad in Southeast Asia

Meet Alex, a freelance graphic designer about to spend six months working from laptops and cafes across Thailand, Vietnam, and Indonesia. Alex’s entire business is in one backpack—a powerful laptop, a pro-grade camera, and a handful of other expensive gadgets. The biggest threat isn't just a sprained ankle; it's a stolen computer, which means no income for weeks.

For someone like Alex, a generic, off-the-shelf policy won't do the trick. The search needs to focus on plans built for long-term travelers and remote workers.

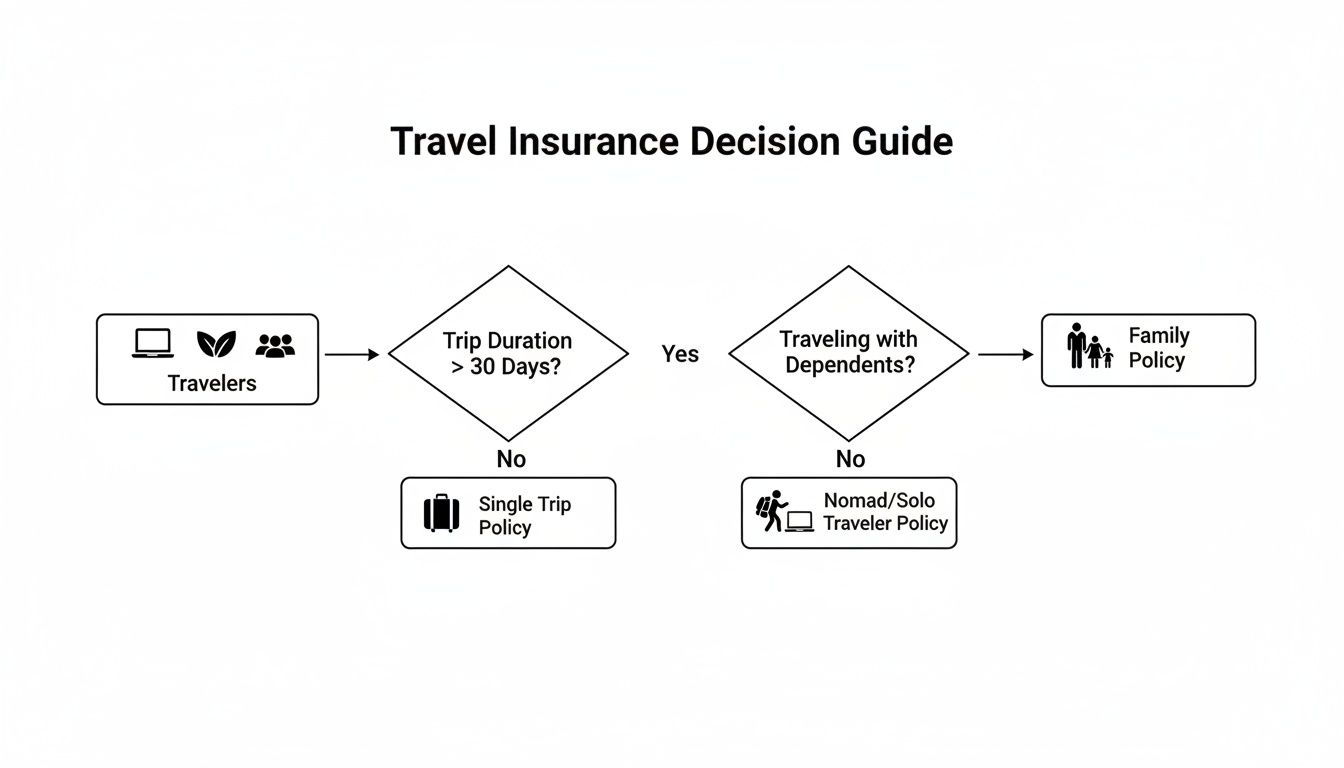

- Long-Stay Coverage: Most standard policies tap out after 30 or 60 days. Alex needs a plan specifically designed for continuous travel for six months or more, one that doesn't force a trip home to keep the coverage active.

- High-Value Electronics Protection: What good is a $2,000 baggage limit if the fine print caps any single item at $250? That’s useless for a professional. Alex must find a policy with a per-item limit of at least $1,000 to $1,500 to properly protect the tools of the trade.

- Scooter and Motorbike Use: Zipping around on a scooter is part of the Southeast Asia experience. But many basic insurance plans have a glaring exclusion for accidents on two-wheeled vehicles. Alex has to find a policy that includes this or offers it as a reasonably priced add-on.

For a digital nomad, insurance is more than just a medical safety net—it's business continuity insurance. The right policy protects their ability to earn a living anywhere in the world, making high-limit tech coverage and long-stay validity the absolute cornerstones of their plan.

The Eco-Volunteer in the Amazon

Next up is Maya, a conservationist volunteering for three months with a non-profit deep in the Amazon rainforest. Her days involve trekking through dense jungle and helping out at a small, local clinic. The medical facilities are rudimentary at best, and the nearest real hospital is a tough, day-long journey away.

Maya's insurance needs couldn't be more different from Alex's. Her entire focus is on what happens during a serious medical emergency in a very, very remote place.

- Massive Medical Evacuation Limits: This is Maya's number one, non-negotiable feature. A standard $250,000 evacuation limit could be wiped out by a complex, multi-stage airlift from the jungle. She should only be looking at policies that offer $1,000,000 or more for medical evacuation.

- Hazardous Activity Coverage: Believe it or not, some insurers might classify her volunteer work—which involves manual labor and trekking—as a "hazardous activity." She needs to dig into the policy details to make sure her specific duties are covered, and be ready to purchase an adventure sports rider if they aren't. If you're planning a similar trip, our guide on volunteering abroad for cheap can help you prepare for this kind of amazing experience.

- A Rock-Solid 24/7 Assistance Team: When you're in a crisis with spotty communication, the quality of the 24/7 assistance team is everything. Maya should research the reputation of the assistance company the insurer partners with. They will be her lifeline, the ones coordinating everything if the worst happens.

The Family on a European Road Trip

Finally, let's look at the Chen family—two parents and two young kids on a month-long road trip through Italy and France. They've prepaid for their rental car, booked non-refundable hotels, and bought tickets to museums and attractions. For them, the risks are all connected. If one person gets sick, the whole trip grinds to a halt.

The Chens are looking for a policy that wraps the whole family in a blanket of coverage, protecting their finances and saving them from logistical nightmares.

- Strong Per-Person Benefits: It’s critical to compare "per-person" versus "per-policy" limits. A good family plan provides high coverage limits for each family member, not one single pot of money that could be drained fast if two people need help at once.

- Rental Car Collision Damage Waiver (CDW): Many credit cards offer this, but a primary CDW baked into a travel insurance policy is often better. It saves them the headache of filing a claim with their personal car insurance back home and can make the whole process smoother if their rental gets dinged.

- Generous Trip Interruption Coverage: Imagine one of the kids gets a sudden ear infection and the doctor says they can't fly for a few days. That's a domino effect of cancelled plans. A policy with 150% trip interruption coverage is a game-changer. It doesn’t just refund their prepaid, unused costs—it also helps cover the sky-high price of last-minute plane tickets home.

Walking through these different trips makes one thing perfectly clear: a great travel insurance comparison isn't about finding the "best" policy out there. It's about finding the best policy for your trip. It’s about choosing a plan that understands your risks, protects what matters most to you, and gives you the peace of mind to go have an incredible adventure.

Your Personal Travel Insurance Comparison Matrix

It’s easy to get lost in the theory, but this is where the rubber meets the road. You’ve seen what makes a policy tick and how it plays out in the real world. Now, let’s get you from passively browsing to actively choosing the right plan with confidence. Forget having a dozen tabs open trying to remember which quote said what; this is about creating your own command center.

We're going to build your personal travel insurance comparison headquarters. It's a straightforward but incredibly effective way to line up policies side-by-side and see exactly what you're getting. Think of it as a custom-built tool designed to highlight what matters most for your specific journey.

Building Your Custom Comparison Tool

Grab a notebook or fire up a simple spreadsheet. Create a column for each policy you’re looking at and rows for the most important features. This simple act of organizing the information will instantly reveal the strengths and weaknesses that are so easy to miss when you're just clicking around websites.

At a minimum, your rows should include:

- Emergency Medical Limit: The absolute cap on what the policy pays for medical bills.

- Medical Evacuation Limit: The maximum coverage for getting you to a proper hospital.

- Deductible: What you have to pay out of your own pocket before the insurance kicks in.

- Trip Cancellation & Interruption: The percentage of your prepaid, non-refundable trip costs they'll cover.

- Baggage (Total & Per-Item): The limits for your gear if it gets lost, stolen, or damaged.

This kind of visual breakdown makes the decision process so much clearer.

As you can see, your travel style—whether you’re a long-term nomad, a volunteer, or traveling with family—points you toward very different coverage priorities.

Personalizing Your Matrix for a Perfect Fit

Now for the magic. This is where you tailor the matrix to your life and your trip. Add custom rows that reflect what you’ll actually be doing and what you’re bringing with you. The goal here is to create a filter that immediately flags the policies that truly get you.

Your matrix isn't just about comparing dollar amounts. It's a tool that forces you to ask better questions and define what peace of mind really means for this specific adventure. It turns a ridiculously complex decision into something you can actually manage.

Think about adding these personalized rows:

- "Pre-existing Condition Waiver?" (Yes/No): This is non-negotiable if you have any health issues.

- "Specific Activity Covered?" (e.g., Scuba Diving, Scooter Rental): List out the adventures you’re planning. Don't assume they're included!

- "CFAR Upgrade Available?" (Yes/No/Cost): Check if you can add "Cancel For Any Reason" coverage and what it costs.

- "Electronics Per-Item Limit": Absolutely essential for digital nomads, photographers, or anyone traveling with a pricey laptop.

Once you fill this in, the best choice often becomes surprisingly obvious. This systematic travel insurance comparison puts you back in the driver's seat, moving you from feeling overwhelmed to feeling totally in control. This level of organization with your insurance goes hand-in-hand with smart financial planning on the road. For more on that, check out our guide on 7 travel budget categories that save you money in 2025. Consider this matrix your final step to locking in not just any policy, but the right one.

Smart Ways to Save on Your Travel Insurance

Finding the right travel insurance shouldn't break the bank. The real goal isn't just to snag the cheapest plan, but to find the smartest one—a policy that gives you total peace of mind without eating into your adventure fund. It’s all about getting incredible value for your money.

It’s tempting to just click "add insurance" when you're booking a flight, but that's almost always a mistake. Those convenient, one-size-fits-all plans often lack the serious medical or evacuation coverage you might actually need. A far better move is to use a dedicated travel insurance comparison site. These marketplaces let you stack up dozens of options at once, so you can easily see who offers the best coverage for your trip at a price that makes sense.

Find the Right Policy Type and Save Big

If you're on the road more than twice a year, an annual multi-trip policy is your secret weapon. Instead of buying a new plan for every single trip, you get one that covers you for a full 12 months. The upfront cost feels bigger, but it almost always saves you a ton of money in the long run compared to buying individual policies each time.

Even if you're only planning one big getaway, you can still find great deals by comparing single-trip plans. These policies make up 61% of the market and typically cost just 4-8% of your total trip price. That's a tiny investment to protect yourself from major travel headaches. You can find more interesting stats about the travel insurance market over on imarcgroup.com.

The real value of insurance isn’t the price tag—it’s the disasters it protects you from. A plan that costs a little more but gives you $500,000 in medical evacuation coverage is infinitely better than a cheap one with a $50,000 limit when you're in a real emergency.

Buy Early and Check Your Existing Perks

Here’s a simple trick that costs you nothing: buy your policy as soon as you make your first non-refundable deposit, like booking your flights. The price doesn't change, but your coverage window gets way longer. This immediately activates crucial benefits like trip cancellation, protecting your investment for all those months leading up to your departure.

Finally, take a quick look at the benefits you might already have. Many premium credit cards come with built-in travel perks, like rental car insurance or coverage for delayed baggage. They're never a substitute for a real travel insurance policy (especially for medical emergencies!), but knowing what you're already covered for can stop you from paying for the same thing twice.

Combine these strategies, and you’ll find a solid policy that lets you explore the world with confidence. To make your travel budget stretch even further, don't miss our guide full of essential budget travel hacks.

Navigating the Claims Process Like a Pro

A travel insurance policy is just a promise on paper until the moment you actually need it. When something goes sideways on the road, knowing how to file a claim with confidence is what turns that piece of paper into a genuine safety net. This is where your investment pays off, but only if you’re ready.

Filing a claim isn't about luck; it’s all about being organized and moving fast. The second an incident happens—a medical emergency, a stolen backpack, a canceled flight—your first call should be to your insurer's 24/7 assistance line. They’ll point you in the right direction, but the job of collecting proof falls squarely on your shoulders.

Your Essential Documentation Checklist

From the moment something happens, you need to think like a detective. Your mission is to build such a solid case for your claim that there's simply no room for doubt. Every receipt, every report, every email is a crucial piece of your puzzle.

Here’s what your claim file should always contain:

- Medical Incidents: You'll need detailed invoices from the hospital or clinic, a formal report from the attending doctor outlining the diagnosis and treatment, and all receipts for prescriptions.

- Theft or Loss: A police report, filed within 24 hours of the incident, is an absolute must-have. Insurers are incredibly strict about this. You'll also need proof of ownership for your valuables—think original receipts, photos of you with the item, or even credit card statements.

- Cancellations or Delays: Keep all official communication from the airline or travel company explaining the reason for the disruption. You'll also need your original and rescheduled itineraries, plus receipts for any extra expenses you had to cover, like meals or a hotel room.

The single biggest mistake travelers make is failing to document everything. Without official reports and itemized receipts, your claim is just a story. With them, it's a fact the insurer must address.

Sidestepping Common Claim Denials

Insurance companies aren't out to get you, but they absolutely will deny a claim if your paperwork is a mess or you miss a deadline. Knowing the common pitfalls is your best line of defense.

The most common reasons for rejection are often frustratingly simple to avoid. Missing that 24-hour window to file a police report after a theft is a classic mistake. Another is failing to get a detailed medical report, which leaves the insurer guessing about whether the treatment was truly necessary.

For lost valuables, the lack of proof of ownership is a frequent deal-breaker. You have to prove you owned the camera or laptop you're claiming. A brilliant travel habit is to keep digital copies of receipts for all your expensive gear in a cloud drive—it's a simple step that could save you thousands.

When you treat the claims process with the seriousness it deserves, you put yourself in control. This preparation turns a crisis into a manageable problem, ensuring you can confidently use the protection you paid for and get your adventure back on track.

Your Top Travel Insurance Questions, Answered

Even the most seasoned travelers have questions. It’s only natural. Let's clear up some of the most common uncertainties so you can finalize your choice with complete peace of mind and get back to the fun part—planning your adventure.

When Is The Best Time To Buy Travel Insurance?

Simple answer? As soon as you make your first major trip payment. Whether that's booking your flight or putting down a deposit on a tour, locking in your insurance right away is a game-changer.

Buying early means your trip cancellation coverage kicks in immediately, safeguarding the money you've already spent. Plus, for many of the best perks—like a pre-existing condition waiver or the coveted Cancel For Any Reason upgrade—insurers require you to buy within a tight window, usually 10-21 days of that initial deposit. Don't wait.

Does Travel Insurance Cover Pre-Existing Medical Conditions?

This is a big one, and the answer is: it depends, but you often have a great option. While most basic plans will exclude pre-existing conditions, many top-tier policies offer something called a pre-existing medical condition exclusion waiver.

This waiver is your golden ticket. To get it, you typically need to buy your policy soon after booking your trip and be medically stable enough to travel at the time of purchase. Dive deep into the policy details on this—it’s a non-negotiable for so many of us.

Understanding the difference between what your credit card offers and what a dedicated policy provides is one of the most important steps in any travel insurance comparison. One is a nice perk; the other is a true safety net.

What Is The Difference Between Travel Insurance And Credit Card Protection?

It’s tempting to rely on the "travel protection" offered by your fancy credit card, but they are worlds apart from a real insurance policy. Card benefits are a nice bonus, but they typically offer drastically lower coverage limits for medical emergencies, trip cancellations, and lost gear.

Here's the most critical distinction: credit cards almost never include emergency medical evacuation. An airlift out of a remote location can easily soar past $100,000, and that’s a bill no one wants. Think of your card’s perks as a light supplement, not a substitute for a comprehensive safety net.

Ready to explore the world with the confidence that you're fully protected? At Travel Talk Today, we provide the insights and tools to help you design trips that are as smart as they are inspiring. Start planning your next adventure today!